President targets multiple-home ownership as stock rally reshapes investment flows

President Lee Jae Myung has declared war on housing speculation, using X as both a megaphone and a pressure tool.

“For the sake of a sensible and prosperous nation, I will rein in, by any means, real estate speculation that can ruin the country,” Lee wrote in an X post on Feb. 3.

In just over a month, he has posted more than two dozen times on real estate, framing it not as a narrow property issue but as a broader distortion of the national economy.

“Housing speculation robs young people of hope and harms the country,” he said.

And he appears prepared to back up his rhetoric. Lee has cast housing as part of a broader push to reset entrenched systems and made clear that property would be no exception.

“Buying or selling homes is a personal freedom,” he wrote. “But whether that decision becomes profit or loss will be determined by government policy.”

He even put his own home up for sale in late February, saying he did so out of a sense of duty to “set an example for everyone.”

The message is already rippling through the market. In February, the Bank of Korea’s house-price outlook index posted its sharpest drop since mid-2022.

Weekly data from the Korea Real Estate Board also showed prices edging down in Seoul’s most expensive districts — including Gangnam, Songpa, Yongsan and Seocho — the first decline there in about two years.

Is housing market really speculative?

Ending speculation is the most urgent national task

Lee’s description of Korea as a “property-speculation republic” reflects a long-running debate over whether housing has become less a place to live than a vehicle for investment.

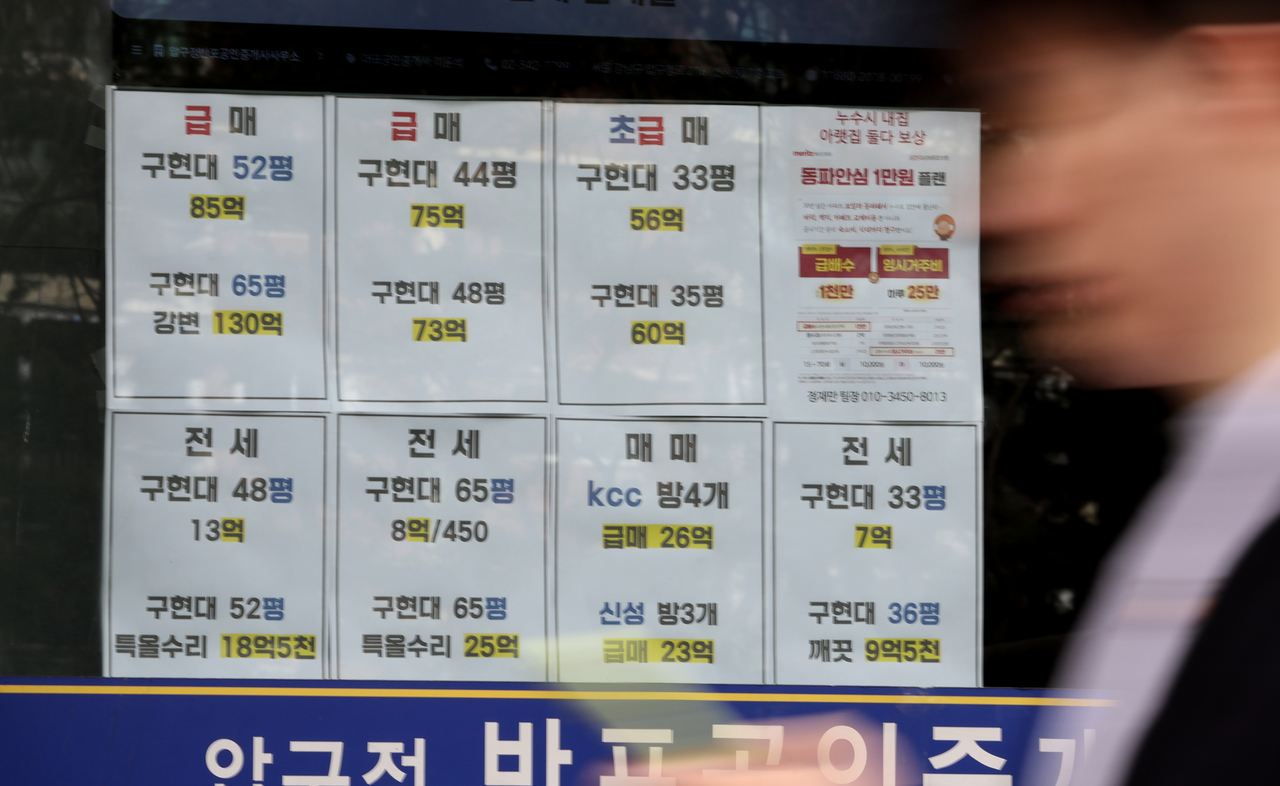

One reason often cited is Korea’s jeonse system. Instead of paying monthly rent, tenants put down a large lump-sum deposit, which landlords can use to finance investments — often purchases of other homes.

Jeonse has also enabled what is widely known as "gap investment," in which buyers acquire homes with relatively little equity input by relying on tenants’ deposits to cover much of the purchase price. In many cases, the deposit can amount to more than half the value of the home.

Multiple-homeownership is a key focus of Lee’s effort to rein in speculation. About 15 percent of homeowners own two or more properties, while the top 20 percent of those owners control nearly 80 percent of housing assets by value, according to a recent Oxfam Korea report.

Transaction patterns point in the same direction. Ministry data show home sales rose 13 percent nationwide in 2025, compared with 36 percent in Seoul and 43 percent for Seoul apartment deals, underscoring how heavily speculative demand is concentrated in apartments and in the capital region.

Still, the diagnosis is contested. Kwon Dae-jung, a professor at Hansung University, cautioned against portraying Korea as uniquely speculative.

“It’s hard to say Korea is especially speculative. Cities like New York or those in Australia have at times seen even larger price increases,” he said, noting that home prices tend to rise as urban economies expand and competition for housing intensifies.

Kwon also stressed the need to distinguish speculation from investment.

“Speculation usually refers to short-term buying and selling to capture capital gains,” he said. Long-term ownership aimed at generating rental income, he added, is closer to investment.

What is normal?

Is the housing market normal now?

Lee argues that speculation has deepened structural imbalances across the economy.

“Home prices and rents have soared so high that young people are giving up on marriage and births are falling, putting the country itself at risk,” he wrote.

Seoul’s housing burden remains severe. The city’s price-to-income ratio stood at about 13.9 in 2024, meaning a home for the average household costs nearly 14 times its annual income.

Korea’s household balance sheet adds to the distortion: Property accounts for roughly three-quarters of household wealth, far more than in countries such as the US or Japan, where financial assets play a larger role. Property dependence also rises with wealth, reinforcing the sense that housing is central not only to shelter but also to wealth accumulation.

Debt is another risk. Korea’s household debt amounts to about 90 percent of gross domestic product, among the highest of any advanced economy. Relative to income, leverage looks steeper still, with household liabilities equal to roughly 175 percent of disposable income.

The imbalance is also geographic. Across OECD countries, housing in large cities was on average 86 percent more expensive than in very small cities in 2023, but in Korea the gap was 211 percent — the widest in the sample and the only one above 200 percent.

Why now?

Normalizing the property market is easier than fixing the stock market

Lee’s real estate offensive is not unfolding in isolation. It has gathered force alongside — and in part because of — a dramatic rerating of Korea’s stock market.

The Kospi topped Lee’s 5,000 target in January, less than a year into his presidency, and crossed 6,000 in late February, a surge his camp has cast as proof that capital can be redirected from property into equities.

One industry expert, who requested anonymity, said the rally likely sharpened the government’s timing.

“The fundamental idea of this administration is to reduce multi-home ownership and channel those funds into the capital market,” he said. “But because the stock market rose more sharply than expected, they also see a risk that the money could flow back into housing.”

On that reading, the crackdown is partly preemptive, meant to stop a new wave of wealth from flowing into Seoul apartments while also drawing out temporary supply through sales by multiple-home owners.

October’s mortgage tightening was an early signal. The government’s Oct. 15 package capped mortgage amounts by price tier and tightened leverage rules in Seoul and other regulated areas, explicitly targeting high-priced, investor-led buying.

With the Kospi at record highs — achieved in part on expectations tied to his policies — Lee is explicitly pointing investors toward a different asset class.

“In the past, real estate was the only investment option. Now there are alternatives,” he wrote.

Where it’s headed

Selling will be better than holding out, and sooner the better

The next credibility test comes on May 9. The government says the temporary deferral of heavier capital-gains taxes for multi-home owners will end then, though it has added some exemptions: contracts signed by May 9 can still close within four to six months, depending on district designation, under the old tax treatment.

Lee has paired that deadline with unusually direct pressure.

“Even for the sake of the government’s credibility, we cannot allow those who held out to end up better off than those who sold before May 9,” he said. “We will make sure that choices made in defiance of government policy, or out of distrust of it, will not turn into profit.”

Once the suspension ends, the current 6-45 percent basic capital gains tax could rise to as high as 82.5 percent of profits for owners of three or more homes. Finance officials are also reviewing tighter treatment of loan rollovers and refinancing for existing multi-home borrowers, which would make waiting out the policy shift harder even without new purchases.

Lee has also floated phasing out capital-gains advantages for registered rental homes after mandatory rental periods end. Within the ruling party, lawmakers have proposed more controversial steps, including stronger holding taxes and narrower capital-gains exemptions, though those would require broader political consensus.

Supply is the longer game: 1.35 million housing starts in the Seoul metropolitan area by 2030, plus a 60,000-unit fast-track plan on underused urban sites.

Kwon said the overall direction of Lee’s policy was right in seeking to curb speculative demand and reduce multi-home ownership.

“But if too many abrupt changes are pushed through at once, that is not reform but revolution,” he said.

“In cities like Seoul, prices are bound to keep rising, as they do in other major global cities, so the answer is to strike a balance: Tax unearned gains appropriately while making homeownership possible for ordinary households.”

jwc@heraldcorp.com